Financing Real Estate in France as a Foreigner: What You Need to Know

For foreigners aspiring to invest in French real estate, one common question arises: “How can I finance my property in France?” France’s property market is highly attractive, offering diverse opportunities from quaint countryside homes to luxurious city apartments. However, financing a real estate purchase as a non-resident involves unique considerations. Here, we delve into the most common methods, their costs, and a practical example to guide you in making an informed decision.

1. Equity Release on Property Back Home

For British and American nationals, equity release from a property in their home country is a popular financing option. This strategy involves borrowing against the value of an owned property to free up capital for investment in France.

Advantages:

Quick Access to Funds:

- Equity release is relatively straightforward and doesn’t depend on navigating French banking systems or regulations.

Costs:

- The average cost is approximately 5-7%, which is high for a loan and average to low for equity gain.

Considerations:

- The cost of equity release is non-negligeable and often based on variable rate.

- It requires substantial equity in your home country property.

2. Sale of Shares or Financial Assets

Selling shares, stocks, or other financial assets is another commonly used method. This approach is particularly appealing to investors who have already realized substantial gains in financial markets.

Advantages:

Ease of Mobilization:

- Liquidating financial assets can often be done swiftly, ensuring funds are available when needed.

High Opportunity Cost:

- While these assets typically generate annual returns of 7-14%, the potential loss of future returns should be weighed against the stability and long-term appreciation of real estate investments.

Considerations:

- Timing the sale is critical, especially in volatile markets.

3. Obtaining a Mortgage in France

Foreign buyers can secure a mortgage from French banks, though the process may involve more scrutiny compared to local buyers. The average loan-to-value (LTV) ratio is around 70%, depending on the buyer’s profile and the property being purchased.

Key Metrics:

Loan Tenure and Rates: A 20-year loan with a fixed rate typically costs less than 4.00% per annum.

LTV Ratio: Foreign investors generally need to contribute a downpayment of at least 30%.

Advantages:

- Leverage: Financing allows you to retain liquid capital for other investments or emergencies.

- Favorable Rates: French mortgage rates are among the most competitive globally.

Considerations:

- French banks assess factors like income stability, creditworthiness, and the property’s location.

- Documentation requirements can be stringent, requiring proper planning and expertise.

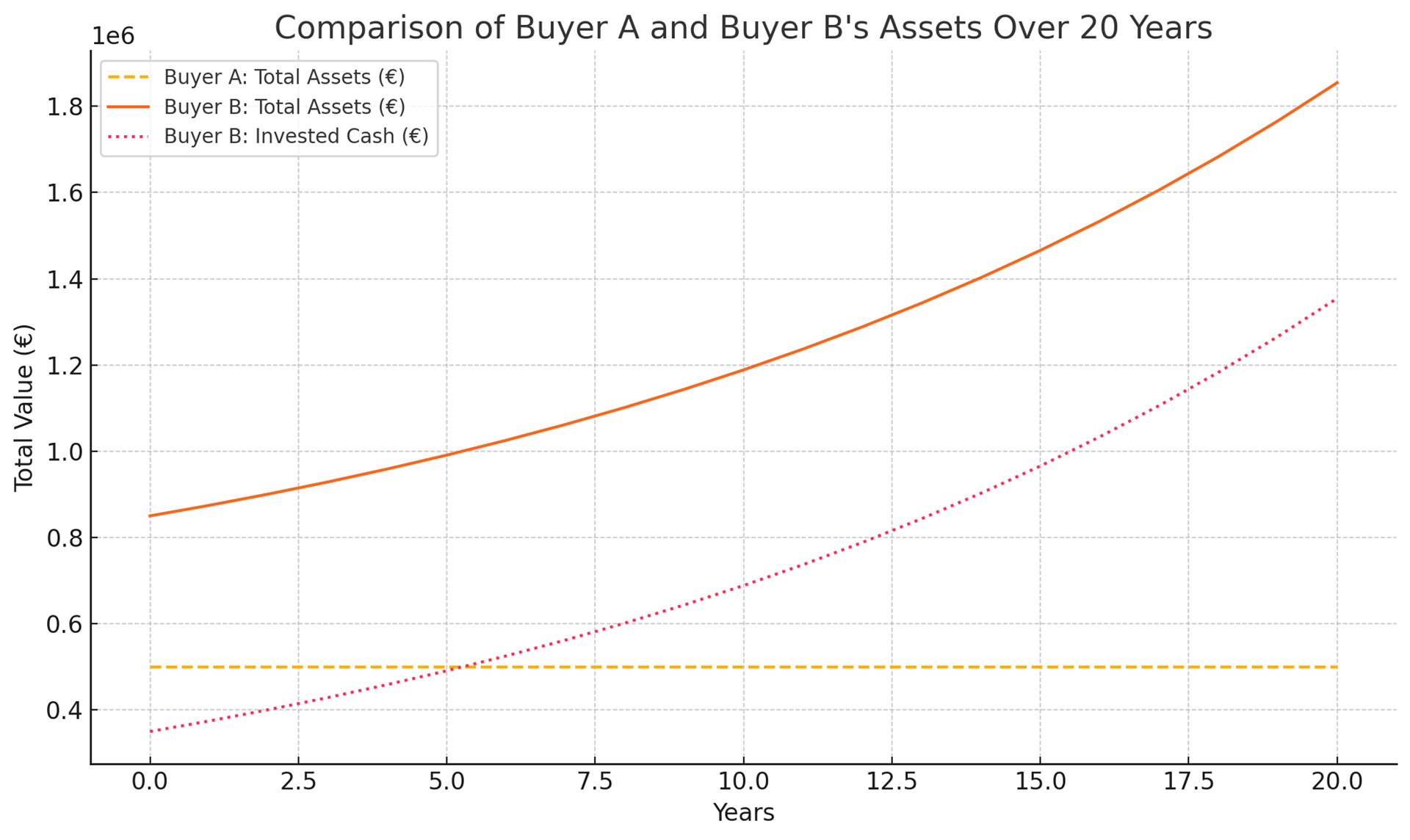

Practical Case Study

Let’s compare two buyers who purchase the same property valued at €500,000 under different financing strategies.

Buyer A: A cash buyer who invests the full €500,000 upfront. While avoiding interest payments, Buyer A ties up all available funds into the property, with no other cash for investments. Over 20 years, the property appreciates, but no additional wealth is generated beyond its value.

Buyer B: A leveraged buyer who puts down €150,000 as a downpayment and finances the remaining €350,000 through a mortgage. Over 20 years, the loan costs an additional €150,000 in interest (at a 4% fixed rate). However, Buyer B keeps the €350,000 that wasn’t used for the property invested in financial markets, earning an average return of 7% per annum.

Results After 20 Years:

- The property’s value remains constant for both buyers.

- Buyer A owns the property outright but has no surplus cash.

- Buyer B owns the property and has approximately tripled the initial investment of €350,000, demonstrating the power of leveraging.

Conclusion

Financing real estate in France as a foreigner offers multiple pathways, each with its own pros and cons. Cash purchases provide simplicity and freedom from interest payments but limit potential returns. On the other hand, leveraging through a mortgage or equity release can maximize overall wealth, provided it is managed prudently.

For investors considering French property, understanding these options and tailoring the approach to personal financial goals and risk tolerance is key. Working with experienced advisors in real estate, finance, and local regulations can make the journey smoother and more profitable.

Lead photo credit : Photo: Freepik

Share to: Facebook Twitter LinkedIn Email

More in finance, mortgage, property

Related Articles

Leave a reply

Your email address will not be published. Required fields are marked *

REPLY